Home Equity Loan Advantages: Why It's a Smart Financial Move

Home Equity Loan Advantages: Why It's a Smart Financial Move

Blog Article

Demystifying the Certification Process for an Equity Funding Authorization

Navigating the certification procedure for an equity loan authorization can often appear like deciphering an intricate problem, with numerous aspects at play that identify one's qualification. From strict credit report requirements to careful home assessments, each action holds value in the lender's decision-making process. Comprehending the interplay between debt-to-income ratios, loan-to-value ratios, and various other crucial requirements is paramount in protecting authorization for an equity car loan. As we dig deeper into the intricacies of these requirements, a clearer course emerges for potential consumers seeking economic utilize with equity loans.

Secret Qualification Criteria

To receive an equity lending authorization, conference specific crucial eligibility criteria is necessary. Lenders generally require candidates to have a minimum credit report rating, typically in the series of 620 to 700, relying on the establishment. A strong credit background, revealing a liable repayment record, is also crucial. Furthermore, lending institutions evaluate the applicant's debt-to-income ratio, with most favoring a ratio listed below 43%. This shows the customer's ability to manage extra financial debt sensibly.

Moreover, lending institutions review the loan-to-value proportion, which contrasts the amount of the funding to the appraised value of the property. Satisfying these vital eligibility requirements enhances the possibility of securing approval for an equity funding.

Credit Score Score Relevance

Credit rating usually range from 300 to 850, with greater ratings being much more positive. Lenders usually have minimal credit history demands for equity lendings, with scores over 700 typically thought about great. It's vital for applicants to review their credit rating reports frequently, looking for any mistakes that could negatively impact their ratings. By keeping a good credit report with prompt costs settlements, reduced credit history usage, and accountable loaning, candidates can improve their chances of equity financing authorization at competitive prices. Comprehending the relevance of credit rating scores and taking actions to boost them can considerably impact a customer's financial opportunities.

Debt-to-Income Ratio Analysis

Provided the crucial duty of credit report scores in establishing equity loan approval, one more essential facet that lenders examine is an applicant's debt-to-income ratio analysis. A reduced debt-to-income ratio suggests that a customer has more revenue offered to cover their financial obligation repayments, making them a much more appealing candidate for an equity funding.

Debtors with a higher debt-to-income ratio may face difficulties in safeguarding authorization for an equity finance, as it recommends a greater danger of skipping on the car loan. It is necessary for applicants to evaluate and potentially decrease their debt-to-income ratio prior to using for an equity car loan to increase their opportunities of authorization.

Property Assessment Needs

Assessing the worth of the property with a detailed assessment is a fundamental action in the equity lending approval process. Lenders require a building assessment to ensure that the home offers adequate security for the loan quantity asked for by the consumer. Throughout the residential property evaluation, a qualified evaluator assesses numerous variables such as the residential or commercial property's problem, dimension, place, similar home values in the area, and any type of unique attributes that might impact its general worth.

The property's appraisal value plays a crucial function in establishing the optimum amount of equity that can be borrowed against the home. Lenders generally need that the appraised value fulfills or goes beyond a certain percentage of the lending amount, called the loan-to-value ratio. This proportion helps alleviate the lending institution's danger by guaranteeing that the home holds adequate value to cover the financing in case of default.

Eventually, a complete residential or commercial property evaluation is crucial for both the loan provider and the consumer to properly assess the building's worth and establish the feasibility of giving an equity financing. - Home Equity Loan

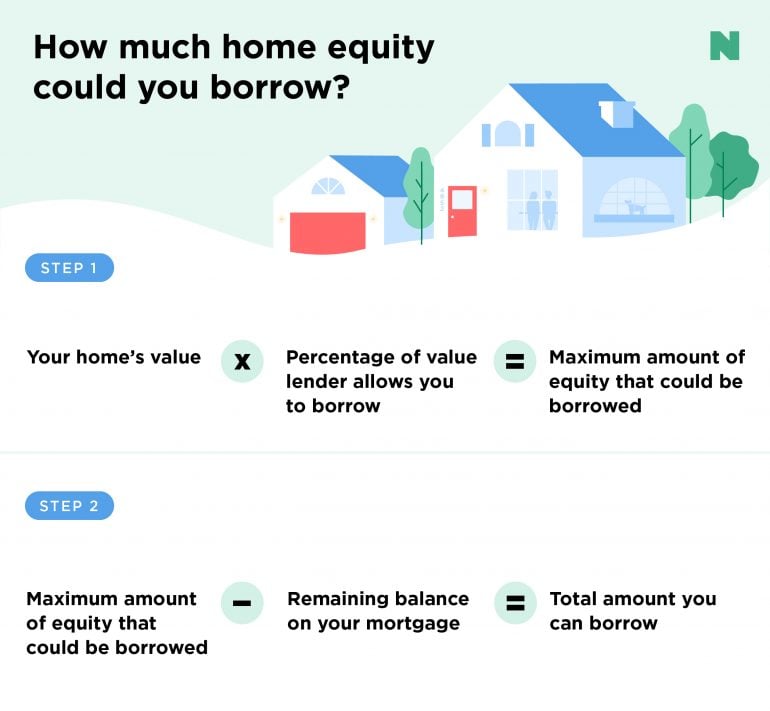

Recognizing Loan-to-Value Ratio

The loan-to-value ratio is a vital financial metric used by loan providers to evaluate the risk related to supplying an equity car loan based on the residential or commercial property's evaluated worth. This ratio is determined by splitting the amount of the car look at here loan by the evaluated worth of the building. For instance, if a property is appraised at $200,000 and the finance amount is $150,000, the loan-to-value ratio would certainly be 75% ($ 150,000/$ 200,000)

Lenders make use of the loan-to-value proportion to identify the degree of threat they are taking on by giving a lending. A greater loan-to-value ratio indicates a higher danger for the lender, as the debtor has much less equity in the property. Lenders commonly prefer lower loan-to-value ratios, as they give a pillow in instance the consumer defaults on the financing and the residential property requires to be marketed to recover the funds.

Debtors can likewise benefit from a reduced loan-to-value proportion, as it might lead to much better loan terms, such as reduced rates of interest or reduced fees (Alpine Credits Canada). Comprehending the loan-to-value proportion is crucial for both loan providers and customers in the equity car loan authorization procedure

Verdict

To conclude, the credentials procedure for an equity financing approval is based on vital qualification criteria, debt score relevance, debt-to-income proportion evaluation, residential or commercial property appraisal needs, and understanding loan-to-value proportion. Meeting these standards is crucial for protecting authorization for an equity lending. It is crucial for consumers to meticulously evaluate their monetary standing and residential property value to raise their opportunities of authorization. Recognizing these elements can aid people browse the equity finance approval process better.

Recognizing the interaction in between debt-to-income ratios, loan-to-value proportions, and other vital requirements is critical in protecting approval for an equity finance.Offered the vital function of credit rating scores in identifying equity finance approval, one more essential aspect that loan providers assess is an applicant's debt-to-income proportion evaluation - Alpine Credits Canada. Debtors with a greater debt-to-income proportion may encounter difficulties in protecting approval for an equity car loan, as it recommends a higher threat of skipping on the lending. It is crucial for applicants to assess and potentially decrease their debt-to-income proportion before applying for an equity finance to raise their chances of authorization

In conclusion, the qualification procedure for an equity funding authorization is based on key eligibility standards, debt rating importance, debt-to-income proportion analysis, building evaluation requirements, and understanding loan-to-value ratio.

Report this page